By MPA 11 Sep 2023

https://www.mpamag.com/au/mortgage-industry/market-updates/business-lending-on-the-rebound/459018

Australia’s economy is like a boxer that’s been knocked down a number of times but refuses to give up. Battered by the heavy blows of the pandemic, which brought lockdowns, job losses and business closures, the economy rallied post-COVID as consumer spending grew, travel and immigration increased and the cheap cost of capital drove demand for loans. Then it was back on the ropes again as the invasion of Ukraine; rising interest rates and inflation; higher supply chain problems and labour shortages hit hard.

While the economy may be down, it’s definitely not out. When it comes to commercial lending, the sector has taken its fair share of jabs, but it’s bouncing back, according to leading commercial lenders, a commercial aggregator and brokers who attended MPA’s annual Commercial Lending Roundtable at Crown Sydney’s Silks restaurant.

Participants included Cory Bannister, senior vice president and chief lending officer, La Trobe Financial; Karen Carter, general manager, commercial third party, BOQ Business; Anita Hyde, former head of specialised and private, commercial broker, NAB; Ryan Harkness, managing director, ORDE Financial; Michael Moloney, general manager, Resimac Asset Finance; Barry Saoud, general manager mortgage and commercial lending, Pepper Money; and Stephen Scahill, group executive commercial, LMG. Representing brokers were Jean-Pierre Gortan, managing director of Simplicity Loans & Advisory, and Sukhi Singh, director of Infinity Finance Solutions.

Among the issues discussed were the effects of higher inflation, interest rates, supply chain problems and other challenges on commercial lending; how SME finance, asset finance and commercial property were faring; the opportunities for brokers; diversification; and future growth areas in commercial finance. Q: What shape is the commercial lending sector in, and how is it being affected by rising interest rates, inflation, supply chain issues and other challenges? Michael Moloney (pictured below) of Resimac Asset Finance started the conversation by focusing on asset and equipment finance. He said SMEs were in a good position. “They’ve certainly got their eye on what’s happening over the horizon with rates and unemployment, but from an SME lending perspective, we believe they’re in good shape,” Moloney said. “We’re not really seeing supply chain issues as such an issue these days.”

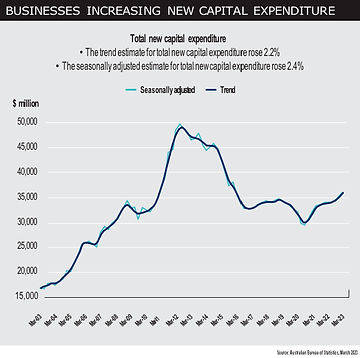

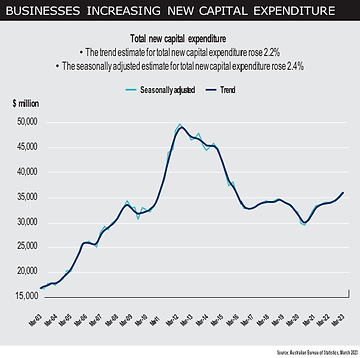

He said the latest ABS data showed that private new capital expenditure was higher in the March 2023 quarter than one year prior in March quarter 2022. “We’re reasonably buoyant about that, but we accept that there are headwinds on the consumer side,” Moloney said. “We’re well aware that the cost of capital has gone up, so we’re certainly looking at the timing of equipment [purchases] and the cost, but overall things are generally positive.” Anita Hyde (pictured below) said that at NAB “we’re cautiously optimistic about the commercial lending sector and the economy more broadly, but we’re seeing emerging pockets of concern”. She said there had been a pullback in discretionary spending on household furniture and electronics, and more broadly from branded goods to market goods that were available. “So while we’re seeing consumption growth slow, the economy outlook more broadly remains resilient.” Karen Carter said BOQ Business had seen businesses rebuilding their inventory over the last year, and “there may be less demand for inventory finance this coming year”.

“Despite immigration rising and not as much demand, there are still staff shortages playing out,” she said. “We do expect there will be a bit of a downturn in business lending for the next few months while people restock and wait for interest rates to settle.” Pepper Money’s Barry Saoud (pictured below) agreed with the term “cautiously optimistic” but said the concern now was about the rising cost of capital. “With 12 interest rate increases in such a short space of time, I think it’s going to put significant pressure on some of the SMEs looking forward,” he said. “Couple that together with some of the wage increases and the cost of goods, I think that’s a concern.” However, Saoud said small businesses were very resilient and would pivot and look at different parts of their business to thrive. “They’ve got to look at what are the opportunities out in the marketplace while the economy is quite strong and take advantage where they can.” Asked if he’d seen a drop-off in commer- cial loans, Saoud’s response was no.

“Not a drop-off – we’re still in the growth phase of commercial lending,” he said. “We think the opportunity for us is more about our diversification and how we’re supporting brokers.” Resilience was the key phrase, said Ryan Harkness (pictured below) of ORDE Financial. “I think Australian SMEs have been performing very well to date. They’ve been very prudent.” Harkness said that by making prudent decisions, SMEs were making sure they set themselves up to be sustainable in tough times. They also realised that there were plenty of opportunities to scale and excel. “Whenever there’s uncertainty, that creates opportunity,” Harkness said.

“A lot of Australian SMEs are actually taking a stance that certainty will return, but every time you think it’s getting closer, it seems to be a step further away.” He said business certainty would arrive at some point in 2023, with businesses just needing “to get through the coming months”. “Our book is performing extremely well,” Harkness said. “Our SME commercial book is even outperforming our residential portfolio, which really goes back to the resilience of the borrowers.” La Trobe Financial’s Cory Bannister (pictured below) shared similar views and said that while there had been challenges, resilience was also the word he would use. “What we’re seeing is some opportunity where perhaps borrowers are faced with technical issues rather than actual fundamental serviceability issues,” he said.

Bannister said rising rates were causing second-order impacts, and whether these were seen in interest coverage ratios or review clauses, they were brought about by rapidly rising interest rates.

“So we’ve got an influx of borrowers who are looking to have to take a defensive step to play offence, so they have to go sideways or slightly back to be able to go forward with what their intent is.”

Commercial borrowers seemed optimistic about the longer-term outlook, Bannister said. On a macro level, “things looked pretty solid”, but commercial property, including offices, was a worry due to the work-from-home phenomenon. But he pointed out that about 1.5 million additional overseas migrants were due to arrive in Australia over the next five years, and while all the media attention had been on the housing shortage, these people also needed places to work.

“The narrative is tilting now – from where it was previously about the office being a doom and gloom story, to actually there’s going to be a demand for office space,” Bannister said. “I think the medium-to longer-term outlook is quite encouraging for retail and other sectors as well.”

Stephen Scahill (pictured below) said broker aggregator LMG was confident about commercial finance. “For new funding, we’re in a good space. There’s a lot of capital out there, and whilst credit appetites might change, and some might push more into non-banks, I think the customer has the opportunity to make that decision and say, ‘Yes, this makes sense for us to obtain that capital’.” LMG’s biggest area of concern was what Bannister touched on: existing customers who have loan facilities that they may be forced to move from. “They’re in a position where they have to take a deal that’s probably not as good as what they’re on today,” Scahill said. “That could bring with it some challenges.” Commercial finance broker Sukhi Singh (pictured below), director of Infinity Finance Solutions, said clients were doing quite well and looking forward to the future. However, for some there was uncertainty, with the most recent interest rate rises sapping their confidence.

“They’re saying, ‘What’s the plan now? Where do I go?’ Half a per cent [rate increase] is not a big number for a lot of those clients, but it seems to be a moving feast at the moment – they don’t know where it’s going to get to,” Singh said. He said some of Infinity’s clients who work in wholesale had been talking about hiring people six months ago, but that had changed. “I spoke to one client recently, a major import facility, who said, ‘I might have to reduce 5% of my salesforce if I’m to maintain profitability in business’. “Those challenges are very real for the SME market. It comes down to profitability, for them to retain staff and run a successful business,” Singh said. Jean-Pierre Gortan, managing director of commercial brokerage Simplicity Loans & Advisory, said that at the risk of contradicting Scahill, he believed there was a lack of liquidity in certain sectors of the commercial space – “whether that’s illiquidity or whether that’s credit rationing, or whether that’s just credit appetite”.

“Whilst there’s probably demand from the borrower side there, there is difficulty especially in certain sectors, such as land, to find the right capital partners; not a lot are really interested in that,” Gortan said. This could be due to uncertainty over land value and “feasibility blowing up due to construction costs that are too high”.

Q: Broker question from Jean-Pierre Gortan: Are there issues as far as capital inflows? Are you just being more selective as to the kind of credit risks that you’re taking, or is it a combination of both? Are you rationing capital? Is that a short-term approach to wait and see what’s happening with all these rate rises, or is it a fundamental shift in your appetites?

Bannister said there was certainly no credit rationing at La Trobe Financial, and volumes were peaking for the lender at present. “We’re taking a cautious outlook on various segments of the market as you would expect, given the current macro conditions,” he said. But in terms of development and commercial finance in general, there had been no change in appetite at all. “In fact, we’re seeing more opportunities now in that space than ever before, and our asset mix continues to normalise post- COVID,” Bannister said. “For a while during COVID, there was a purposeful tilt to resi- dential, due to the uncertainty in the commercial sector, but it continues to normalise as demand increases for products such as construction development. “I agree with you, JP, that there’s been a tightening of liquidity in the market generally – private lenders have largely vacated that space for the time being due to the new challenges,” he added. There were also more commercial oppor- tunities arising for non-banks due to clients struggling with traditional bank ICR cove- nants and review clauses.

Saoud said “there’s absolutely no credit rationing” at Pepper Money. “We see there’s significant liquidity out in the market, and we’re there to take advantage of it.” He said Pepper Money had been in the commercial lending space for three years, and in the last three months it had taken a significantly expansive approach, “whether it’s credit policy, loan limit or security type”. “We’re looking to really grow in the space. We wouldn’t see any type of tightening of credit at the moment. We’re more focused around how do we take advantage of the right borrower cohorts and those right segments.” Hyde agreed and said it was not so much about capital but credit appetite. “So it’s the commercial property fundamentals that ring true in the market. If you’ve got a strong asset, a strong developer, that’s ringing true, and we’re fully supportive. Where the caution lies is when you’ve got developers that are new or not familiar in the market, the appetite there is more cautious.” Gortan (pictured below) said he thought that during the COVID period NAB was “anti-retail”, and he asked Hyde if this was still the case. Hyde responded by saying NAB had “opened up” when it came to retail.

“So we are comfortable [with lending for retail], depending on the location,” Hyde said. “When it comes to office space, we know there are ongoing challenges with working from home for CBD property, but we’re seeing selected opportunities with an increase in office space needed in all major cities in the next 12 months.” Harkness said ORDE Financial was seeing a lot of opportunity. He said brokers asked lenders, “Are there certain industries you won’t support?” But he pointed out that too many banks took a generalised view of lending, compared to ORDE. “We take a case- by-case assessment of every application based on the underlying characteristics of the indi- vidual, and this is highly important.” He said that just because a specific industry had not succeeded during COVID, that didn’t necessarily mean a specific business also wouldn’t succeed. “That’s become a really key area of focus for us – the credit solution approach on an individualised basis, investing a little time to get to know each application.” Harkness said a lot of this work happened presubmission between BDMs and brokers – “putting our heads of credit into scenarios to give comfort to brokers that that scenario will actually go from start to finish”. ORDE Financial had commenced as a new, broad-spectrum residential and commercial lender three years ago and established a strong funding platform to deliver an ever-extending commercial product range to support brokers. Harkness said that, far from rationing capital, ORDE Financial envisaged significant further extensions of its funding capability.

He said there was considerable misunder- standing in the market of what was commer- cial and what was residential. He gave the example of developers buying land with a plan to build apartments or townhouses in five years’ time – these were small developments, two to four properties, and because there was a commercial intent, there was not a lot of lending support in the market. “Supply chain issues and construction are starting to iron out … we look at it from a resi- dential lens, understanding what the developer is trying to do; look at the underlying securities that are the true residential value and try to support them where we can.” Carter (pictured below) said BOQ’s approach was to have a strong capital position. “We’ve been very deliberate on that. We do focus lending growth towards our niche markets, particularly the SME, health and agribusiness industries.” Q: How do you work with brokers to meet the needs of commercial finance clients while also supporting brokers diversifying into this space?

Scahill said that at LMG the most important thing was to understand the intent of the broker business. “Not all broking businesses are set up to support commercial customers, so we need to give them solutions,” he said. “We develop referral programs where they’ve got someone that can either handle the transaction for the broker or guide them through the transaction in a co-pilot manner if their journey is to learn commercial finance.” For brokers wanting to get involved in commercial deals, Scahill said training was crucial. “I think some of the failings with training in the past have been that it’s quite theoretical, that you go, you learn the fundamentals of commercial finance, and then off you go and ‘good luck’.” Schill said LMG was trying to take a systematic approach as it did in residential lending so that training took place within a supported platform. In the area of lending for commercial auto equipment, Moloney said Resimac loans were solely originated through the broker channel. He said Resimac had staff across Australia to help brokers with scenarios on a daily basis, “whether it’s in a broker’s office or over the phone”.

“We’re going live with a new system, which will make applications quicker and also decisions quicker,” Moloney said. He had also seen one aggregator boast of a 20% increase in commercial brokers over the past year, and that was a great positive that proved the pathway was working. Harkness said that commercial lending provided an amazing opportunity for ORDE Financial and brokers; in the residential space brokers enjoyed around 70% market share, but in commercial “we’re nowhere near that”. “Brokers should be doing 70% of commer- cial and 70% of residential, and we think lenders have a big part to play in that,” he said. “We spent a lot of time speaking to brokers prior to launching ORDE Financial. One thing they were focused on was product diversity.” Commercial lenders must show consistency of service, including time and solutions-focused outcomes, Harkness said. “What they [brokers] really wanted is a lender who would always help support them, work for a credit solution and make their credit team available. “That was the key thing that we listened to – all the ORDE credit team are available; we put our heads of credit in scenarios, giving direct access to any broker. This means you’re speaking to the end decision-maker; if they say yes, we’ll find a solution for you.” Harkness said this approach meant brokers could provide certainty to their customers.

Education was also important, as well as supporting brokers on their loan deals, he said. “All of our credit analysts’ phone numbers are available on the ORDE website, and we say to the brokers, call them because we want to educate as part of the process.” “Building on that,” Hyde said, “when you’re talking about commercial finance client needs, it’s about connecting with an established network. So, for example, you’re financing an industrial warehouse, but you also need the invoice finance to stock the warehouse, and then you need the forklifts and the trucks. It’s about connecting the broker with internal networks that can assist with those additional client needs as well.” Carter said BOQ Business provided a commercial broker portal for brokers to access, featuring niche industry standards and summaries. “It helps the brokers under- stand the fundamentals that we’re looking for in the end deal. We also have questionnaires for brokers to ask customers and servicing spreadsheets as well, WALE and interest cover calculators, etc. “We’re definitely doing a lot in the education space around our niche markets. For example, if you’re going to lend to a doctor, what does the average doctor earn? What is the fair market value EBITDA multiple for purchasing a practice?” Carter said BOQ wanted to share this information so brokers were informed. BOQ educates brokers on specifics, including the cost of fit-outs, right down to the nitty-gritty of where electrical power points should be located.

“We’re just trying to make sure that brokers understand the industry because it’s easy to go out and say, I can get you 100% of fit-out, commercial lending or goodwill lending, but if the fundamentals of the deal and understanding of the industry aren’t there, it can become hard for the client,” Carter said. Saoud said everyone was talking about broker diversification, the importance of supporting brokers and having stronger relationships with customers. “We’re not only talking about selling them their home loan but how do you support them with their commercial lending or asset finance needs.” He said those gathered around the table, whether banks or non-banks, were really strong on having accessible credit teams, supporting brokers by workshopping deals, and trying to get the speed to yes on credit decisioning and a more predictable and consistent outcome. “Where we can probably look to support brokers better is about how they farm for their business, because we can all do well on credit,” Saoud said. “But I think for brokers, how they deepen relationships, market to their existing customer base and how they really focus on diversification is key.” Saoud said aggregators did this well through data insights and analytics. “That’s where the big growth will come – taking that broker base from where we’re currently writing less than 40% of commercial loans into the 70% and above.” Scahill said it was about the same people making the decision. “So the person deciding how to access their capital for commercial also owns a home and most likely has dealt with a broker.”

“It’s ensuring there’s that consumer awareness that brokers can offer all forms of facility as opposed to just residential lending,” Scahill said. “That’s the message we want to get out there. We’re huge believers in the growth of broker share in commercial lending over the next four to five years; we think it’ll nearly double.” Q: Broker question from Sukhi Singh: Where is the differentiation and recognition from lenders that takes into account those brokers who specialise in commercial and instead of just originating the loan are in effect managing the process due to their expertise? Singh said brokers who specialised in commercial finance could recognise when a certain deal would not fit a specific lender’s credit appetite and would take it elsewhere, saving that lender time and money. Bannister answered the question by saying that La Trobe Financial tackled this in a couple of ways. “La Trobe Financial segments our credit teams between residential and commercial, but equally, the people that are coming to us on a regular basis will have access to a dedicated credit team as well, so there’s a familiarity there for the brokers and credit staff, and that’s important.”

On an industry level, Bannister said the non-bank had taken a different approach. “We’re trying to purposely lower the [broker] barrier to entry by having products and docu- mentation requirements that are approachable and easy to use. We acknowledge that that’s not easily achievable in all aspects of the commercial market, so I certainly under- stand why the banks perhaps wouldn’t have it that way.” Bannister conceded there were two schools of thought about whether there should be a high barrier to entry for brokers into commer- cial lending, with experienced brokers wanting a higher barrier. “That’s totally appropriate when it comes to dealing with complex products with lenders that require a lot of ratios and complexity.” But La Trobe Financial wanted to see the broker channel prosper and the commercial broker market share get closer to the residential market share of 70%. The company wanted to play its part in assisting brokers on products that were reasonably non-complex, by reducing barriers to entry. This included having no specific accreditation requirements and using a credit analyst to train the staff and salespeople who are educated on these loans. Harkness said ORDE Financial had been able to build its technology platform from the ground up to be highly focused on digital, supporting and enabling credit analysts. This was particularly true once operating at the scale volumes that had impeded other lenders in recent years. “Slightly different to Cory’s model, we actually like our credit analysts to do commercial and residential together,” he said.

“For the past three years, the new ORDE Financial platform has been delivering two-day service standards consistently across residential and commercial.” Harkness said many clients had both resi- dential and commercial loans, and “splitting that deal with someone looking at the commercial or residential, you might end up with two different outcomes”. “Looking at the deal in totality and understanding the security that we have available enables us to make a decision that’s optimal for the broker and the end client that they’re working with.” He said the non-bank was investing in its technology to bring consistency to credit assessment, not to define the end outcome but to spend more time finding the solution. “More time on the solution means we don’t have to differentiate between brokers; we want to give all brokers two-day turnarounds. We think we can deliver service to all and help them win clients.”

Hyde said NAB had lifted its broker stand- ards for entry higher in regard to experience in commercial. “At NAB we’ve got a really big support network, and we’ve expanded our small busi- ness BDMs for this reason – for those entering the market to provide more support in the small business space,” Hyde said. “We’ve also launched more dedicated broker bankers … we have lifted the criteria. We’re also providing more support for those brokers that do want to enter.” Scahill said there was a systemic challenge – “so many good bankers are now brokers”. He said in many cases a more experienced broker would put the credit memo together and give it to a less experienced banker to vet and handle the credit. “There is an opportunity for experienced commercial brokers to be dealing direct to credit, getting that submission straight through, stripping cost out of the processing time and cost for the bank. Equally, there’s an opportunity for more reward to the broker to reflect those savings.”

Scahill said there was an opportunity for the industry to segment, recommend and recognise highly experienced commercial brokers and have a different process for them. At Resimac, Moloney said there was a combination of the digital platform and broker training. “Our portal certainly goes straight through to credit – that’s where the training piece comes in. But if it all goes to the head of credit, that’s also problematic, in my view.” Brokers needed to know what was likely to get approved, so it could be a “cleaner” credit process. “On the lending side, we’re contin- uing to train our credit analysts as well,” Moloney said. Gortan said he had a slightly different perspective: it wasn’t so much about whether a broker knew how to get a loan deal done or get an outcome; “it’s probably more around depth of their actual offering”. “How many lenders they know, what they understand as far as the offering available in the market, and [how they] can get an optimal outcome, not just an outcome,” Gortan said.

“I think that’s the problem with allowing people to dabble. If you’re not doing it every day, you’re not doing it well. I’ve been doing [commercial finance] for about 20 years; I learn every day, and there’s something else that pops up and you go, OK, great – that now becomes an offering in your bag. “Unless you’re actually doing these deals intensively, you can’t be getting the best outcome for your customer.” Carter said BOQ Business’s dedicated, specialist broker team members dealt directly with brokers. “They know what to look for and ask for when they’re having a conversation about SMEs. “I agree with Steven and the two brokers in the room about experience – it certainly gives them a rite of passage to write a deal and send it straight to credit, because you know that the quality of the deals that you’re getting from them is first class, and they’re going to put a good submission together. There should be some consideration from banks in that regard.” Q: How are brokers operating successfully in asset finance? How can lenders assist them in the transition? Moloney said that from a lender’s perspective, brokers should look at the market and figure out “where’s the growth? Where’s the government incentives? Where’s the opportunity?”

“We’ve got the upcoming Olympics in Brisbane. Look what’s going to be happening in the next 10 years; there’s a new airport in Sydney, there’s roads being built every- where,” he said. While some asset finance sectors were not doing so well, brokers and lenders needed to keep their core customers happy. “It’s about being aware of the tax incentives, the right asset write-offs, and electric vehicle tax rebates,” Moloney said. Singh said the customer interface and ease of doing business were highly important. “If it’s a bigger client, we will always have a limit placed with the lender. But for the standalone stuff, it’s how intuitive the interface is – for somebody in office to be able to plug in, get an outcome and then take it to settlement.” Car finance had rebounded in the last 12 months because dealers’ rates had “gone through the roof ”, Singh said. Brokers wanted applications that were easy to originate, he added. “Sometimes a 12-page application is not the right way to go for a $50,000 car: it’s not the right return on time. But there are options in the market where you actually spend half an hour on originating a loan and getting it through.”

Gortan said that as with commercial and residential finance, it was best to use a specialist for asset finance. Simplicity Loans was involved in some simple asset finance such as leasing, but it didn’t specialise in this area. “The brokers that do it all the time have 40 or 50 different offerings; they can deal with all the different levels, and that’s a better outcome,” Gortan said. “Pepper Money and Resimac both have specialist products and service that specific market, and that’s why they get good volumes. Unless you’re actually doing a significant amount of volume and know who all the people are, it’s difficult to come up with an offering.” Simplicity Loans referred asset finance to specialists to get a better outcome for the customer, Gortan said. Saoud said Pepper Money’s asset lending business had been quite successful, especially in the last few years. “We grew last calendar 35 times system growth, and that’s principally around our investment in our digital technology.

“It’s a high-volume business, and you’ve got to make it easy for your brokers, easy for the customers – the time to yes, and that predictability on credit decisioning.” Pepper Money had invested a lot of time in the system, data insights and credit decisioning. “You need that expedited approval – that’s what we know our customers and brokers want,” Saoud said. He agreed it was important to have that segmented service delivery for high-volume brokers who did it well, but said it was also important to have help available for brokers who were diversifying into the space. Scahill pointed out that technology had a big part to play in asset finance. He said there was absolutely no reason why the residential broker experience of operating from their own platform, analysing lender appetites, and saying to clients ‘here are the rates and options’, couldn’t be replicated. “We see that in asset finance – the experience for the asset finance broker, it becomes much more aligned to what happens in residential lending, and it makes it accessible for more brokers,” Scahill said. Asked by Gortan if he knew the depth of the market for broker-originated asset finance deals, Scahill said LMG didn’t have exact figures: for commercial it was at the low 30% mark, but for asset finance it was unknown.

Hyde said the other point to add was about brokers working really closely with clients, particularly at the end of the financial year, to determine businesses’ future plans, taking into account stock delays and perhaps setting up revolving credit limits. “Always ask the question as, to remove that urgent time to yes, instead it’s taking a forward-looking view and saying, ‘let’s leave some headroom in that limit so that you can come back and acquire the asset promptly at a later stage’,” Hyde said. Commenting on specialist lending, Carter said BOQ had looked at how it could service the A-plus clients and give them easy access to money for equipment and cars, fit-outs, etc. “We can do a 24-hour turnaround on that space given our understanding of the industry,” he said. Q: What do you see as the specific growth areas in commercial lending over the next 12 months?

Bannister said there were a number of growth areas La Trobe Financial was looking at. One was commercial property, where clients were running into problems with ICRs. “That’s fertile ground for what are really high-quality customers that are just technically falling outside of a point-in-time criteria. That’s something we’ve got our eyes open for,” he said. Development finance was another area with a “huge undersupply that needs to be addressed”, Bannister said. “We think we’ve got a part to play in that because we’ve got some flexibility and some heft, not in high-rise stuff but we consider loan applications up to $25 million; we can do some good work around that 40- to 50-apartment-space living – there’s great demand for that.” Regarding the level of presales required, La Trobe Financial had some flexibility there, which helped not only with the devel- opment but also with residual stock.

Bannister said the final growth area was build-to-rent, with some larger institutional players recognising the opportunities. He said AFR had reported there would be $10bn worth of build-to-rent by 2030. ‘“We won’t be at the end of the spectrum but certainly on a smaller scale. We’re seeing lots of developers now seeing the strength of rents and the opportunity and benefits to develop and hold for a four- or five-year period.” Harkness said opportunities lay in debt consolidation in the commercial space for SMEs. During COVID, SMEs took out short-term high-interest-rate loans for working capital, and post-COVID to restock and stock supplies and assets. “We think there’s good opportunity, especially with interest rates going up, to support debt consolidation and refinance under simple 30-year mortgages,” he said. “Making sure people are aware that non- banks can do commercial 30-year set and forget.” ORDE Financial wanted to get people to enter commercial mortgages not for short-term benefits but for medium and long- term benefits.

“Having an ICR test at the end of one year is not necessarily reflective of a bad customer. It might just reflect that they haven’t had a chance to reset their rental yield, which they’ll probably get in the next six or 12 months,” Harkness said. “So being able to give customers certainty of long-term view is something that we’re here to support, and that we think there should be greater education on.” He said ORDE was keen to continue supporting brokers to support SMEs. Moloney said waste, water and energy were areas Resimac was heavily focused on. “Some people have a negative view of construction development, but we really like it. If immigration continues the way it’s going, I think it’s certainly a sector we’re focused on.”

Resimac was also looking at all the SMEs that were peripheral to big infrastructure builds and health. “I think there’s a lot of strong sectors, notwithstanding what we see in the current environment. I think there’s some interesting shifts,” Moloney said. Hyde said it was a very exciting time for brokers: there were “a lot of opportunities out there” with housing supply being a major issue at present, including housing for NDIS, which presented construction opportunities. “In terms of office space, we’ll see that likely pivot in the next 12 months as more people return to work,” she said. “We’re seeing more business customers use commercial brokers, which is really exciting for the space.” Singh agreed it was an exciting time. He said one area of expansion for Infinity Finance Solutions was SMSF funding. “So that’s actually come a long way for us in the last two years to a point where it’s becoming a little business within a business for us. That’s something we do a lot and is gaining a lot of traction.” Singh said the brokerage also specialised in childcare finance. “So we’ve got consultants who will find a site and go through the DSCC process, the building lease, etc. You see that whole cycle go through from inception to when it’s finally operating.”

He said childcare appealed to investors because, once the childcare centre was oper- ational, there was no land tax. “Investors in New South Wales hate land tax, so I think that’s a big thing for the clients, and we’re happy to facilitate the same.” Saoud said what Scahill referred to – the growth of broker participation in the commer- cial lending space and how the industry supported it – was first and foremost. “Secondly, there’s a good opportunity in the non-bank space. I think there’s going to be some significant macroeconomic challenges with different lenders acting more conservatively.” Saoud said the challenge for non-banks was how they could be expansive on security types but also credit decisioning. “How do we look behind financials and actually understand the customer and have a commercial approach to that decision?” “That’s where the non-banks are well positioned, given they don’t have a cookie-cutter approach to credit assessment. I think that’s where there’s going to be really significant growth,” Saoud said.

“Given that with the macroeconomic challenges and what’s happening in the SME market, I think you’re going to have to take a little bit more in-depth analysis on your borrower profile.” Gortan said that while brokers who had dabbled a bit in commercial lending over the last few years would go to a lender and could get the loan to stick, “I think the lenders have moved away significantly from that. You need someone that understands the situation, knows something that niche lender will do specifically, that you can’t necessarily just find by walking into a major bank.” There would be opportunities for experienced, specialised brokers, he said. Commenting on ex-bankers who became brokers, Gortan said that while credit skills transferred across the two professions, being a broker was very different. “Because it’s very easy in a bank to say, ‘look, I can’t help you’. As a broker, you don’t have that option. You’ve got to say, ‘OK, well, I can’t get you what you actually want, but this is the best that’s available for you because of these reasons’.

“So it’s going to be a little bit of a purple patch for brokers that specialise in this space, because it’s significantly harder than it was 12 months ago or two years ago.” BOQ Business was specifically seeing growth in health, agriculture and manufacturing. Carter said there had been a bounce back in financials in 2023 for many SME clients, compared to 2022 when profitability was down, affected by COVID. “Our arrears are low. We want to lend; we want to try and open up in the areas that we think are our growth areas and where the niche is,” Carter said. “We’re really excited about what we want to do and how we’re going to play in the market. There’s plenty being worked on at the moment to continually improve our services to the broker industry, because we believe in it so much.” Scahill said there would be broader funding requirements, and brokers would need to search further afield for loan options. “Some of their traditional lenders may not be able to facilitate transactions that they have done in the past. The role we’ve got to play in that is to scour the market, understand the good operators in the different spaces, and make sure that our brokers have access to them.”

That may involve either working with existing partners to try to broaden their credit appetite or looking for additional partners that could facilitate these transactions, Scahill said.